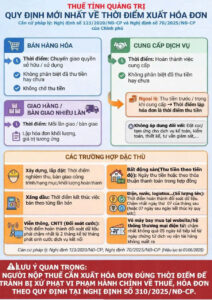

LATEST REGULATIONS ON INVOICE ISSUANCE TIMING & TAX OBLIGATIONS FOR PROPERTY LEASING

(Effective from January 1, 2026)

In order to help enterprises and individuals comply with regulations on invoicing and taxation, the tax authorities have issued several important updates relating to the timing of invoice issuance and tax obligations for property leasing activities , effective from January 1, 2026.

Below is a concise and practical summary for easy understanding and implementation.

I. New Regulations on Invoice Issuance Timing.

(Pursuant to Decree No.123/2020/NĐ-CP and Decree No.70/2025/NĐ-CP – effective from June 01, 2025)

1. Sale of goods

- Invoice issuance time: when ownership or the right to use goods is transferred to the buyer

- Regardless of whether payment has been received

- Enterprises must not wait until payment is collected to issue an invoice

2. Provision of services

- Invoice issuance time: upon completion of the service provision

- Regardless of whether payment has been received

Exception:

- If payment is collected before or during the provision of services → The invoice must be issued at the time payment is received

- This exception does not apply to deposits or advance payments for the following services: accounting, auditing, design, consulting, supervision, etc

3. Multiple deliveries or handovers

- Invoice must be issued for each delivery/handover

- The invoice value must correspond to the actual quantity and value of each delivery/handover

II. Special cases to note

- Construction and installation: Invoice issuance time isthe time of acceptance and handover of completed work, items, or projects

- Real estate (payment by progress): Invoice issuance time is the payment date or as agreed in the contract

- Petroleum and fuel: Invoice issuance time is the end of each sale transaction

-

Electricity, water, logistics (large volumes):

The data reconciliation must be completed no later than the 7th of the following month -

Telecommunications, IT services (charge reconciliation):

No later than 2 months from the month in which the charges arise -

Airline tickets sold via websites/e-commerce platforms:

No later than 5 days from the date the air transport document is issued

🔔 Important note:

Taxpayers must issue invoices at the correct time to avoid administrative penalties in accordance with Decree No.310/2025/NĐ-CP.

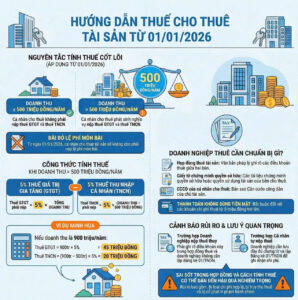

III. Tax guidance for property leasing from January 1, 2026.

1. Core tax principles

-

Revenue ≤ 500 million VND/year:

👉 No Value Added Tax (VAT) or Personal Income Tax (PIT) is required to be paid -

Revenue > 500 million VND/year:

👉 Value Added Tax (VAT) and Personal Income Tax (PIT) must be paid

2. Abolition of business license fee

From January 1, 2026, individuals leasing out property are no longer required to pay the business license fee.

3. Tax calculation formulas (when annual revenue exceeds VND 500 million)

Value Added Tax (VAT):

VAT payable = 5% × Total revenue

Personal Income Tax:

PIT payable = 5% × (Revenue – 500 million VND)

4. Illustrative example

👉 Rental income: 900 million VND/year

- VAT: 900 × 5% = 45 million VND

- PIT: (900 – 500) × 5% = 20 million VND

➡️ Total tax payable: 65 million VND/year

IV. What should enterprises prepare when leasing assets?

- Property lease agreement: Clearly stipulating lease terms and tax obligations

- Documents evidencing ownership or the right to use the property

- Citizen Identification Card (ID) of the lessor

-

Non-cash payment evidence:

Mandatory for payments of 5 million VND or more

V. Risk warnings & important notes

- If the enterprise pays taxes on behalf of the individual, this must be clearly stated in the lease contract

- If the individual pays taxes directly, the enterprise must retain sufficient supporting documents and Form 01/TNDN to ensure the expense is deductible for CIT purposes

Errors in contracts or tax calculations can lead to:

- ❌ Non-deductible expenses

- ❌ Tax arrears

- ❌ Administrative penalties

📌 Recommendation:

Enterprises and individuals leasing out property should review lease contracts, payment methods, and tax obligations to ensure compliance with regulations and minimize tax risks.

- 🔵 Key Highlights of the 2025 Corporate Income Tax Law

- 📦 “THE MOVEMENT OF GOODS” 🎯 IN TAX EXAMINATION AND INSPECTION

- 🔔 UPDATE ON SOCIAL INSURANCE, HEALTH INSURANCE, AND UNEMPLOYMENT INSURANCE CONTRIBUTION RATES EFFECTIVE FROM JANUARY 1, 2026

- Decree 70/2025 on Invoices and Documents: Key Updates to Note

- 🎉🧧 TET HOLIDAY ANNOUNCEMENT 🧧🎉